Just a few years ago, the idea of Meesho, an ecommerce marketplace targeting India’s Tier 2 and Tier 3 cities, outpacing Flipkart to the IPO line would have been laughed away. But that’s exactly what is playing out.

Vidit Aatrey-led Meesho is set for anINR 6,000 Cr IPO (by most estimates), making it one of India’s largest tech listings in the past year.

The potential listing — still some way away — will be a defining moment for India’s new-age ecommerce ecosystem, as it becomes the first horizontal B2C marketplace to go public

Flipkart, whose valuation is roughly 16 times higher than Meesho’s, has been eyeing an IPO for the past 3-4 years, but it’s Meesho that is cashing in on the momentum being seen in the stock markets for new-age companies.

Meesho’s ambition and confidence stems from more clarity in its fundamentals. With its primary business model now set and an in-house logistics business also scaling up, the Bengaluru-based unicorn could set a new benchmark for Flipkart and other marketplaces that follow.

Even though the company has reported heavy losses in FY25, the turnaround seems to be just around the corner. Especially when we look at the margins and unit economics. Let’s dive into how Meesho clawed back from deep losses to come to the verge of break-even.

Meesho’s Growth EngineFounded in 2015 by Vidit Aatrey and Sanjeev Barnwal, Meesho was once seen as the poster child of India’s social commerce boom, before it pivoted decisively in 2023 to a leaner marketplace model. This included cost rationalisation, marketing cuts, shutting down non-core verticals, and several rounds of layoffs.

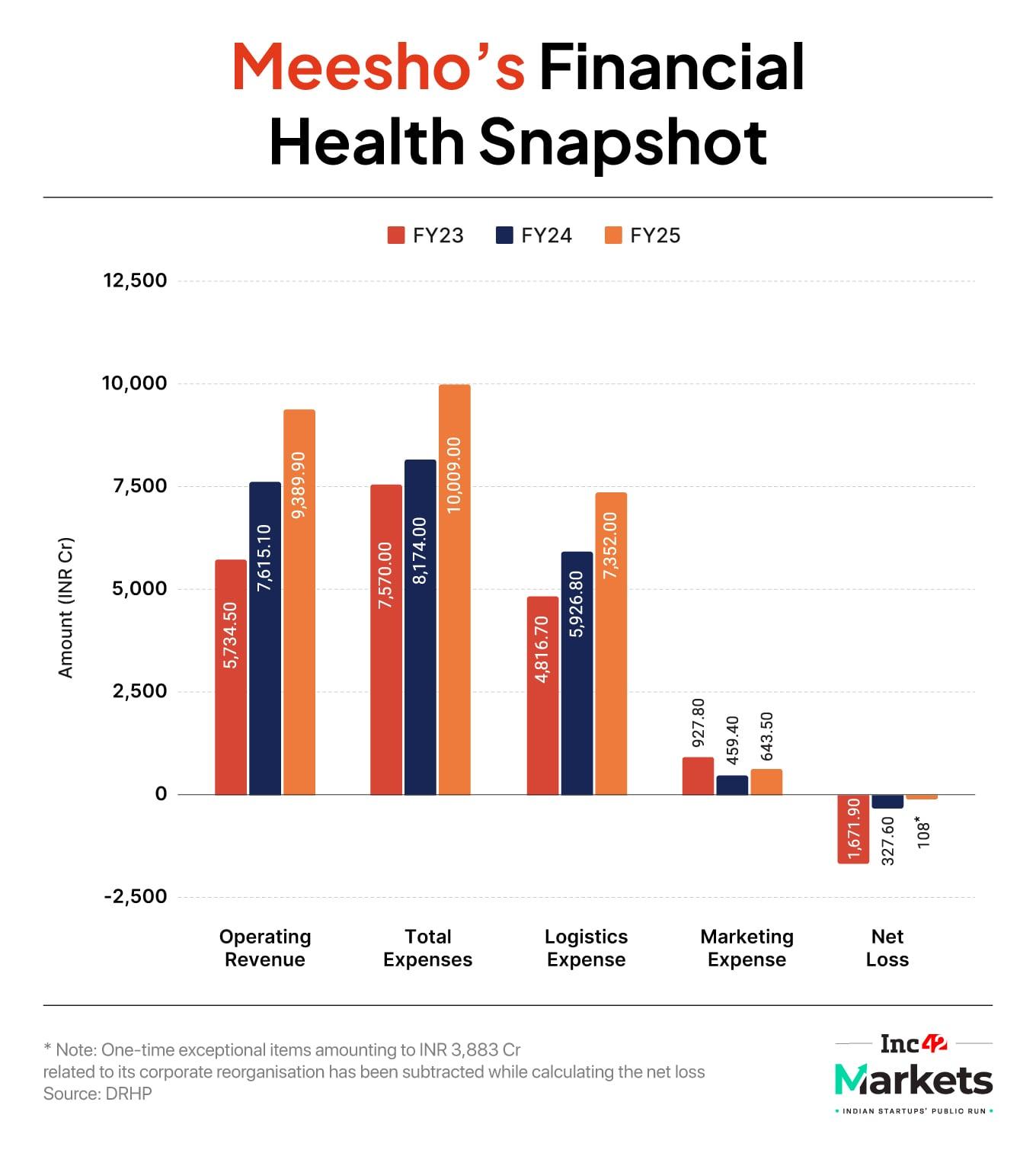

The transformation has delivered results: between FY23 and FY25, revenue from operations surged 64% from INR 5,730 Cr to INR 9,389 Cr, largely driven by its core marketplace and logistics services.

The marketplace primarily caters to a value conscious user base in non metro cities. Of its 213 Mn annual transacting users in the twelve months indeed June 30, 2025, more than 87% came from outside Indian top eight cities, underscoring Meesho’s dominance in rural India’s digital retail landscape.

The platform operates as an orchestrator among four key stakeholders, consumers, sellers, logistics partners, and content creators, without holding inventory or operating warehouses.

The logistics flywheel is centred on Valmo, Meesho’s in-house logistics technology arm, which integrates with third party fleets to optimise first and last-mile deliveries. Higher order density reduces per order logistics cost, while competition among multiple low-cost delivery partners keeps fulfilment prices in check. Meesho claims sellers benefit from these efficiencies by being able to offer the most affordable products, which in turn brings more users and sellers onto the platform.

This flywheel is at the heart of Meesho’s revenue model. The total net merchandise value (NMV) jumped 29% YoY to INR 29,998 Cr in FY25, following 21% growth in FY24. Growth momentum continued into Q1 FY26, with NMV expanding 36% YoY to INR 8,679 Cr, reflecting both rising order frequency and broader product penetration across non-metro markets.

In FY25, content-led commerce generated INR 700 Cr in NMV through Meesho’s marketplace, which increased to INR 946 Cr in just three months ending June 2025.

The startup generates income primarily from services provided to sellers – order fulfillment, return logistics, advertising and data analytics. While FY25 reported a headline net loss of INR 3,914.7 Cr, this was largely due to one-time exceptional items amounting to INR 3,883 Cr related to its corporate reorganisation and reverse flip tax adjustments. Excluding these, Meesho’s net loss stood at a modest of INR 108 Cr.

The discipline is further reflected in Meesho’s adjusted EBITDA margins, which improved -29.5% in FY23 to -2.3% in FY25, signalling the startup’s operating leverage.

More importantly, the startup turned free cash flow positive, a rarity among Indian startups. Meesho’s free cash flow (FCF) improved from a negative INR 2,335 Cr in FY23 to INR 591 Cr in FY25, supported by operational efficiencies, lower fulfilment costs, and growth in NMV.

While there was negative operating cash flow in Q1 FY26, this was attributed to income tax payments tied to promoter ESOP exercises and one-time payments related to the startup’s strategic restructuring.

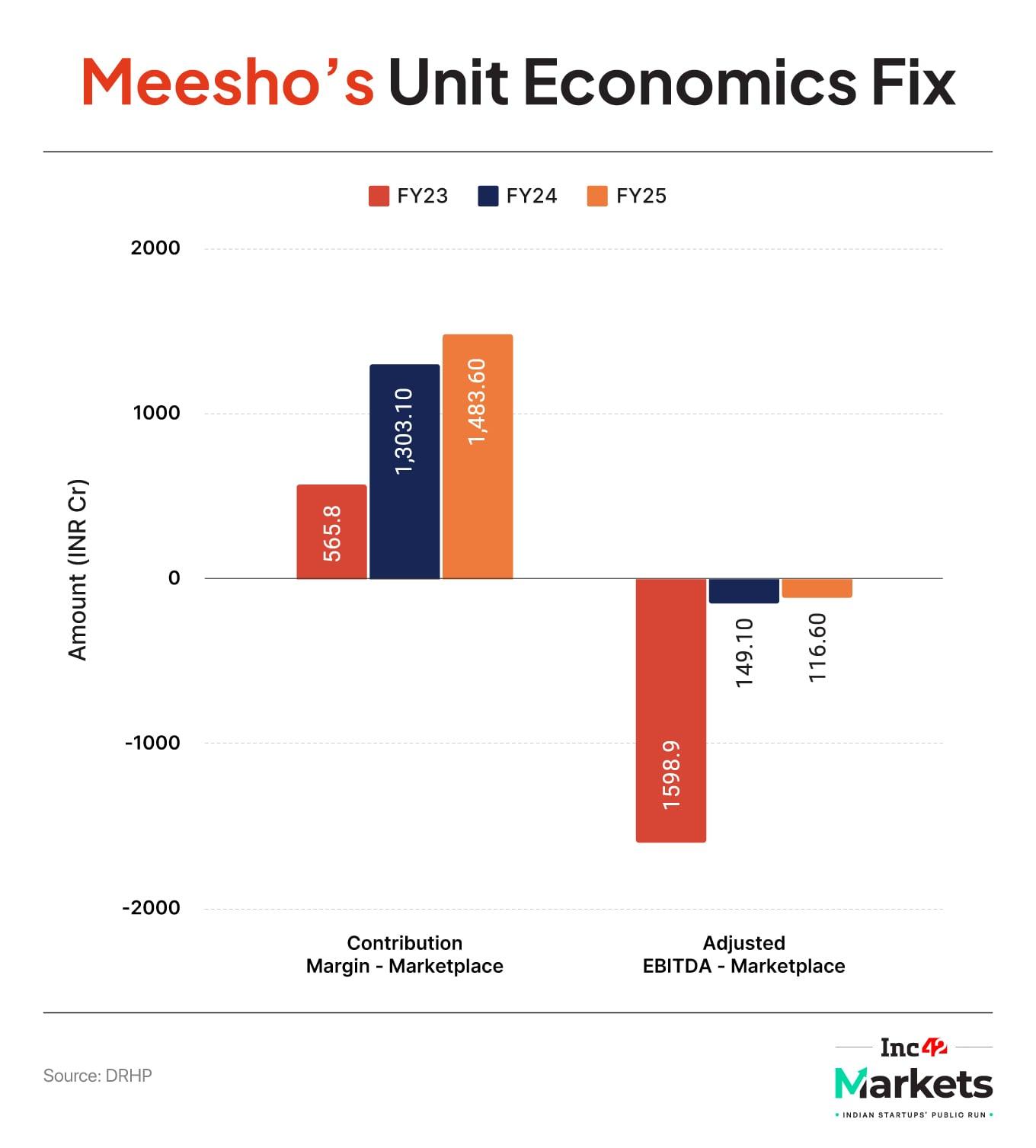

Unit Economics Show Marked ImprovementMeesho’s operating leverage is evident in its improved unit economics. Contribution margin to NMV, a metric that measures profitability before fixed costs, rose from 2.9% in FY23 to 4.9% in FY25, even as the platform expanded into lower-ticket product categories.

This improvement reflects increased efficiency per transaction and tighter cost control across fulfillment and payments, despite a drop in average order value.

Equally significant is Meesho’s declining adjusted EBITDA loss per merchandise unit, down to just 0.39% in FY25 from 8.3% two years earlier. This trajectory indicates that Meesho’s core marketplace is approaching breakeven on an order basis.

As of June 2025, Meesho held INR 539.3 Crin net operating cash and remained debt-free, providing a base for future expansion. While the startup startup may increase marketing spends in FY26 to expand into newer geographies, its core operations remain fundamentally efficient,

But There Are RisksAs usual, Meesho’s DRHP highlights several structural risks that could impact its growth trajectory and profitability.

The most prominent is its thin margin, affordability-driven business model, which limits pricing flexibility. Any increase in logistics, seller commissions, or compliance costs could compress narrow margins further, the company says.

Additionally, Meesho’s heavy reliance on small and medium sellers introduces operational volatility. Many of these sellers lack advanced infrastructure or compliance capacity, raising risks around fulfilment delays, product quality, and adherence to marketplace regulations.

The logistics ecosystem remains another pressure point. Although Valmo has helped reduce fulfillment costs, Meesho still depends heavily on third party logistics providers for execution. Disruptions in these networks, such as strikes, labour shortages, or cost escalations, could affect delivery timeline and customer experience. Maintaining high delivery density is essential to keeping costs low, and any slowdown in order growth could erode this efficiency.

Another risk factor lies in Meesho’s payment composition. The DRHP discloses that 77% of its shipped orders are cash on delivery, which inherently carries higher risk and lower efficiency. Sash transactions recorded a 75% success rate in FY25 compared to 96% for prepaid orders, exposing Meesho to failed deliveries, cash collection delays, and potential losses. The company has already filed cases against certain last mile vendors for non-remittance of COD payments, highlighting the vulnerability of this channel.

Besides this, there is the regulatory exposure. As of June 2025, Meesho reported contingent liabilities worth INR 7,104 Cr, including INR 5,720 Cr income tax dispute and INR 1,169 Cr in vendor related litigation. Adverse rulings in these cases could materially impact near term profitability.

While Meesho’s core marketplace is its cash cow, its new business initiatives such as fintech products, and logistics technology remain in early stages. These verticals will require sustained investment before generating meaningful revenue, potentially straining margins in the short term.

Lastly, players such as Flipkart’s Shopsy, Amazon Bazaar, and Reliance’s JioMart have all begun replicating Meesho’s low cost, seller friendly model, potentially pushing the sector into a deflationary pricing cycle. Sustaining user growth while defending margin, will require constant innovation and sharper execution.

As Meesho gets set to become the ecommerce trailblazer on the stock markets, its biggest challenge will be to maintain profitable growth. Unit economics while currently steady can be disrupted by competition or changing market conditions.

Indeed Meesho has seen first hand that staying alive and surviving in the ecommerce game means being able to adapt. Which is why even though its current course is steady, Meesho will have to endure more than a few uphill journeys even after the momentous occasion of the IPO.

Markets Watch: New Issues, Deals & More- Urban Company’s Shares Dip: Share of Urban Company closed the trading session 3.71% at INR 152 on Friday, after several brokerages shared mixed reactions on the stock’s near term performance.

- Eternal Gets INR 128 Cr GST Demand: Eternal, the parent company of Zomato and Blinkit has received a GST demand order totalling INR 128.4 Cr, including a demand of INR 64.2 Cr and a penalty of INR 64.2 Cr, from Uttar Pradesh’s tax authorities.

- Shadowfax & Curefoods Get SEBI Nod: India’s market regulator SEBI has given a green signal to logistics major Shadowfax and cloud kitchen operator Curefoods. While Shadowfax’s IPO size is not yet public, Curefoods is raising INR 800 Cr via public markets.

- EaseMyTrip To Acquire Stakes In 4 Entities: Travel aggregator EaseMyTrip board earlier this week approved the acquisition of 49% stake each in four companies via share swap.These four companies are Javaphile Hospitality, Doodles, SSL Nirvana Grand Golf Developers, Levo Beauty

- Investor Sells ArisInfra Shares:Amid a surge in ArisInfra shares over last month, investor Premlatha Agarwal offloaded 4.17 lakh shares via a bulk deal with INR 7.4 Cr. The move seems to investors trying to book profit as ArisInfra’s share rally.

Edited By Nikhil Subramaniam

The post From Burn To Break-Even: Meesho Shows Signs Of Turnaround appeared first on Inc42 Media.

You may also like

"Fight is between NDA and Jan Suraaj," reiterates Prashant Kishor

Vidhu Vinod Chopra celebrates 25 years of Hrithik Roshan, Preity Zinta-starrer 'Mission Kashmir'

Inside Shah Rukh Khan's private jet, latest photos go viral

Watch: Desi mom hires band to wake up her kids; video wins internet

JEE Main 2026: Is studying only NCERT enough to crack JEE Main 2026?